How tough was the COVID-19 challenge for collateral managers with the leading OTC market participants? Markets have seen uncertainty, volatility and a move to remote work but for for collateral managers, daily tasks remain the same – just increased in volume and importance. Neil Murphy considers if automation can be a solution to these challenges.

By Neil Murphy, TriOptima

Collateral Managers – similar to their colleagues in Risk Management – like calm & certainty. Within their remit they will often be responsible for validation of large data sets and managing a number of time-sensitive tasks targeted at minimizing counterparty risk. To manage this responsibility their daily checklist will likely include tasks that help them answer the following questions:

• Do we have an accurate record of all our trades?

• Are the trades valued correctly?

• Do our collateral valuations reflect the latest security prices & haircuts?

• Have we made all our margin calls on time?

• Is the collateral proposed by counterparties eligible?

• What is the optimal collateral to pledge to each counterparty?

• Has the correct collateral been received by our custodian?

• What is the cause of any margin call disputes?

In the early weeks of 2020, news of the COVID-19 outbreak was very much a problem far from key OTC markets, and disruption was minimal. Collateral Managers remained calm (and perhaps even unaware). However, by late February the picture was beginning to change. With infections spreading quickly across the globe markets saw a steep increase in uncertainty. And with uncertainty came widespread market volatility, an increase in credit spreads and falling asset prices. Any of these items on their own would typically create a knock-on impact for Collateral Managers; an increase in average margin call size, higher call volumes and potentially larger disputes. None of which would be helpful for a Collateral Manager trying to remain calm.

More bad news for Collateral Managers

By mid-March any semblance of calm was out the window for Collateral Managers. As global infection numbers continued to rise, stock markets experienced record falls, yields on US Treasuries fell to their lowest in history and oil prices declined at a rate not seen in 30 years. Now, more than ever, the role of Collateral Manager was critical.

The daily tasks at hand don’t change for a Collateral Manager during periods of volatility – they simply increase in both volume and importance. Added to an increased workload, many firms would also have had to factor in an increased focus on deadlines & settlement failures. –Throw in unprecedented working conditions and you get a perfect storm.

How big a problem?

TriOptima’s network services – which are used by more than 230 firms to calculate & exchange both VM & IM margin calls, and by more than 2,000 parties to reconcile approx. 90% of all OTC trades –provide an ideal tool to observe the breadth & impact of market disruption. Viewed through this wider lens the impact on Collateral Managers was significant.

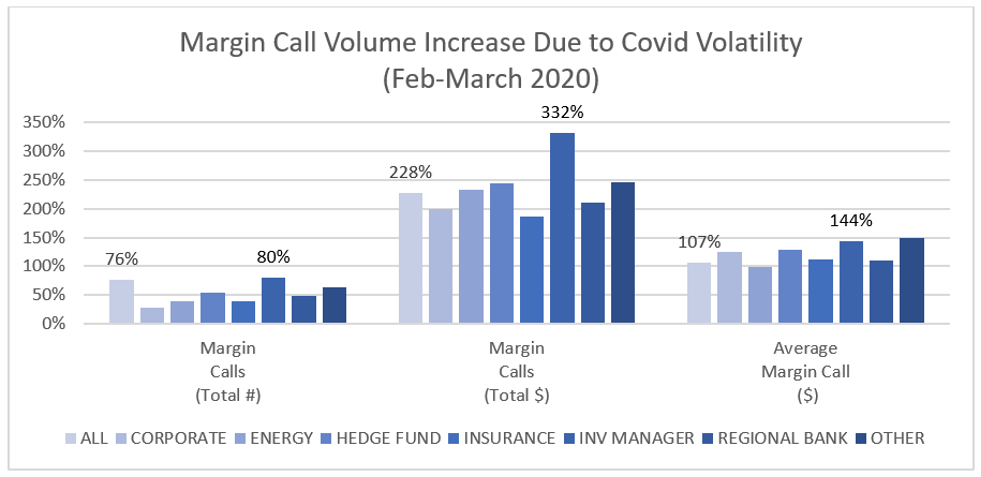

Since the onset of COVID-19 and associated market disruption, TriOptima observed record volumes of both margin call activity and portfolio reconciliation. Average daily margin call volumes seen in triResolve Margin nearly doubled during March from the previous month (which were already trending above average). Added to this, the triResolve portfolio reconciliation service saw record trade volumes and sizeable variation in MTM numbers, both key drivers of margin call disputes. And while spikes in margin call volumes can cause consternation to the Collateral Manager tasked with managing the margin call lifecycle, far more stress comes from an increase in disputes. Not only do these create additional workload, but these are also pointers to increased risk. A trade ‘break’ or a margin call discrepancy potentially indicate uncollateralised credit risk – and like the virus itself, market contagion was a very real risk during this period. While the market was fortunate not to see the widespread failure of firms during this period, the sizeable increase in key metrics will have created new levels of stress for those tasked with managing collateral & reconciliations. Analysis of triResolve Margin activity during the period of March 2020 points to a 76% increase in the average number of margin calls, however looking at the value of margin calls we saw an increase of more than 200%. A deeper dive into the data indicates we should perhaps sympathise with the Collateral Managers working at Investment Management firms – who had to manage the steepest increases across the board; margin call volumes (80%), margin call value (332%).

Source: TriOptima

Business continuity challenges

Unprecedented market turmoil is bad enough but having to manage this while firms simultaneously enacted their business continuity plans, added a new dimension to the challenge facing Collateral Managers. With numerous operational steps in the margin call lifecycle, this typically requires Collateral Managers to access multiple platforms, from Front Office to payments systems. For those firms not able to access all the required systems remotely this required some staff to be physically present in the office in order to keep the wheels turning. In contrast, those firms with web-based systems simply required their staff to have an internet connection at home.

Firms don’t like to shout it loudly, but Excel is still widely used by many firms as a core part of their collateral ‘system’. For those firms still reliant on manual tools such as spreadsheets or email, they were further hamstrung. Unable to respond easily to the increase in margin call volumes they were forced to rely on staff working longer hours. Something already a challenge as many staff juggled working from home with family duties. One Collateral Manager at a large UK hedge fund, dependent on a manual Excel-based approach, described this period as ‘a complete nightmare, with margin call volumes increased by 5-fold’.

In contrast, while we observe triResolve Margin users processing record margin call volumes, we note that they were able to do so inside their normal business hours and within the time constraints documented in their legal agreements. Commenting on the recent period of market turmoil, a spokesperson for Leonteq Securities noted ‘the record volatility levels resulted in margin activity across most of our collateral agreements simultaneously. The use of triResolve Margin’s automated margin call workflow allowed for sufficient capacity for Leonteq’s collateral managers to focus on key controls.’

The ability for our clients to easily cope with the unprecedented volatility isn’t explained simply because triResolve Margin is web-based. Although many users commented this certainly made things easier for them. The operational edge that served users so well during this period came from the combination of a web-based platform and a highly automated workflow. This allowed clients to both send & receive calls, as well as investigate differences in a fully automated way. So, as volatility caused volumes to increase, users weren’t sinking under a need to manually process each margin call or investigate each dispute. Instead, system auto-rules added the required muscle, supplementing the role performed manually at so many firms.

And while auto-rules were widely used by triResolve Margin clients prior to the recent period of market disruption, one knock-on has been an increase in their uptake during recent months. In fact, as the crisis ramped up, our team of Client Managers worked directly with clients to help them quickly activate auto-rules so as to best cope with volumes as they increased from day to day. One client, an international energy firm, moved to adopt auto-rules across their entire portfolio of collateral agreements; allowing both incoming & outgoing margin calls to be completely managed by the system, and alerting the Collateral Manager events which required further analysis & approval. TriOptima analysis of the duration to manage this firm’s entire set of incoming margin calls – measuring time from calls being received to completion of the collateral pledge process – shows the total time required to complete calls fell from several hours to less than 60 seconds. While the associated manual touch-points for the user fell to zero!

A future vision for collateral?

Investigation into, and lessons learned, from the COVID-19 outbreak may be lengthy and painful for governments worldwide. In contrast, the shortcomings faced by some Collateral Managers were hiding in plain sight.

Over-reliance on legacy technology, a near absence of automation at some firms, a lack of investment in keeping up to date with industry best practice and short-termism that sees people thrown at inefficient processes rather than strategic fixes are among the key lessons to be learned. With the twin stresses of volatility and reduced capacity continuing, firms are looking at a ‘new normal’. To best cope, firms should quickly consider moving to update their technology to take advantage of new web-based tools which allow for easy remote access and system inter-operability. Firms should seek to implement high levels of automation, not simply to streamline the processing of margin calls but to achieve optimal risk mitigation. This means a cohesive and integrated approach to both collateral management & portfolio reconciliation, where disputes can be quickly identified and pro-actively resolved.

To find out more about how TriOptima can help, visit https://www.trioptima.com/triresolve/collateral-management/initial-margin/ or contact us at info@trioptima.com.

As the world’s leading and most diverse derivatives marketplace, CME Group (www.cmegroup.com) enables clients to trade futures, options, cash and OTC markets, optimize portfolios, and analyze data – empowering market participants worldwide to efficiently manage risk and capture opportunities. CME Group exchanges offer the widest range of global benchmark products across all major asset classes based on interest rates, equity indexes, foreign exchange, energy, agricultural products and metals. The company offers futures and options on futures trading through the CME Globex® platform, fixed income trading via BrokerTec and foreign exchange trading on the EBS platform. In addition, it operates one of the world’s leading central counterparty clearing providers, CME Clearing. With a range of pre- and post-trade products and services underpinning the entire lifecycle of a trade, CME Group also offers optimization and reconciliation services through TriOptima, and trade processing services through Traiana.

All information contained herein (“Information”) is for informational purposes only, is confidential and is the intellectual property of CME Group Inc and/or one of its group companies (“CME”). The Information is directed to Equivalent Counterparties and Professional Clients only and is not intended for Non-Professional Clients (as defined in the Swedish Securities Market Law (lag (2007:528) om värdepappersmarknaden)) or equivalent in a relevant jurisdiction. This Information is not, and should not be construed as, an offer or solicitation to sell or buy any product, investment, security or any other financial instrument or to participate in any particular trading strategy. The Information is not to be relied upon and is not warranted, either expressly or by implication, as to completeness, timeliness, accuracy, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed. Access to the Information by anyone other than the intended recipient is unauthorized and any disclosure, copying or redistribution is prohibited without CME’s prior written approval. If you receive this information in error, please immediately delete all copies of it and notify the sender. In no circumstances will CME be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the Information. CME and the CME logo are trademarks of CME Group. TriOptima AB is regulated by the Swedish Financial Supervisory Authority for the reception and transmission of orders in relation to one or more financial instruments. TriOptima AB is registered with the US National Futures Association as an introducing broker. For further regulatory information, please see www.cmegroup.com.