As the deadline for USD LIBOR cessation fast approaches, OSTTRA takes a look at the data to get the latest picture of global IBOR reform as of the end of Q1 2023.

By Kirston Winters

OSTTRA through its post trade processing service MarkitWire first facilitated the processing of Secured Overnight Financing Rate (“SOFR”) swaps in July 2018. The first migration of legacy cleared portfolios from USD-LIBOR to SOFR were processed by OSTTRA MarkitWire on the weekend of 22 April 2023. This included trades cleared at Eurex, CME Group and LCH. OSTTRA MarkitWire processed over 250k trades for over 150 counterparties, through its CCP Synchronization service. The main LCH USD conversion and the HKEX conversion is scheduled for 20 May 2023. OSTTRA MarkitWire will also process trades as part of the conversation for dependant currency indices (SGD and THB) in June 2023. The conversion for USD is considerably larger than previous conversions in GBP, EUR, CHF and JPY.

In addition, OSTTRA triReduce has continued to compress legacy USD-LIBOR swaps as part of its compression service. In 2023 OSTTRA triReduce has compressed $8.474 trillion of notional, for 68 entities which also includes dependant currency indices (SGD and THB).

OSTTRA has assessed the data processed by OSTTRA MarkitWire to evaluate the progress of interbank offered rate (IBOR) transition for the $414 trillion single currency interest rate swaps (IRS) market. Analysing market share in USD and CAD between legacy IBORs, overnight index swaps (OIS) and the new risk-free rates (RFRs).

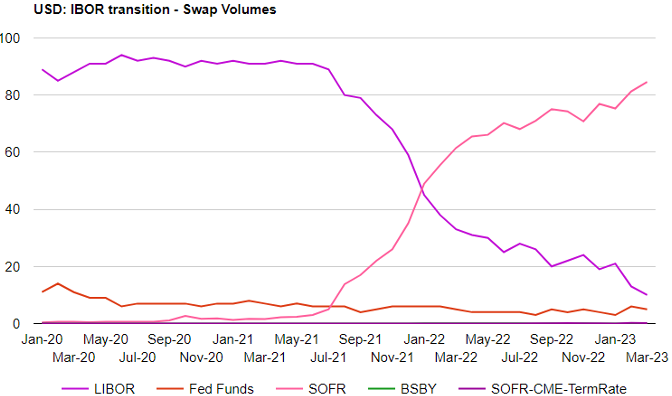

USD swaps

Background:

• SOFR will replace Fed Funds and USD LIBOR.

• There was an initial uptick in SOFR at the end of October 2020 driven by the CCPs switching from Fed Funds to SOFR discounting on 16 October 2020.

• “SOFR first” applied to interdealer swaps from 26 July 2021.

• USD-LIBOR will continue to be published until 30 June 2023.

• BSBY swaps, a credit sensitive rate, have traded every month since September 2021 but remain <0.1%.

• The ARRC approved a Term-SOFR, which has traded every month since June 2022 but remains c. 0.2%.

• The futures market is also progressing, as on April 14, 2023, the remaining open interest of 3-month Eurodollar contracts (post June 2023 expiries) at CME was converted into SOFR equivalent contracts.

• The US Alternative Reference Rates Committee’s (“ARRC”) updated guidelines opens the use of term SOFR versus SOFR basis swaps by hedge funds and fixed rate issuers as demand for hedges grows. The ARRC’s previous guidelines limited the use of term SOFR derivatives to direct hedging of cash products referencing the rate, which resulted in a one-sided market, with term SOFR swaps trading at a premium to compounded-in-arrears versions, which dealers must use to hedge their exposures. With term SOFR emerging as the preferred replacement for USD LIBOR in loan markets, demand for hedges has grown. The ARRC continues to resist calls to allow interdealer trading in term SOFR swaps.

As the deadline approaches SOFR has continued its charge, a new record of 85% of new USD swaps executed in March 2023 referenced SOFR, continuing a month-by-month progression.

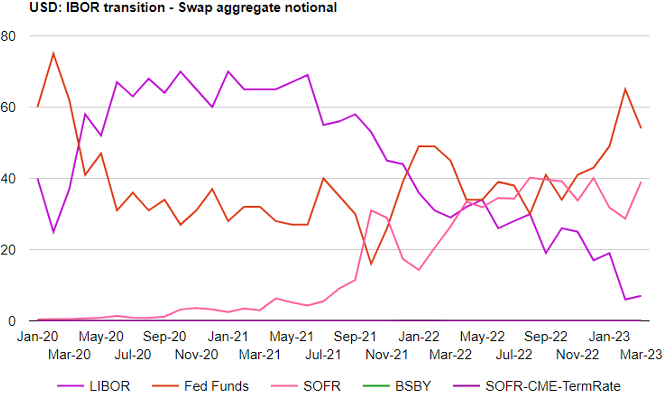

In terms of notional traded, SOFR has been consistently around 40% for the last few months due to Fed funds maintaining around 50% share by notional.

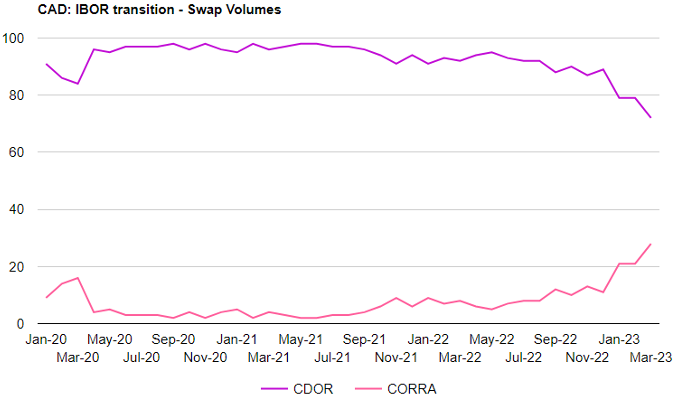

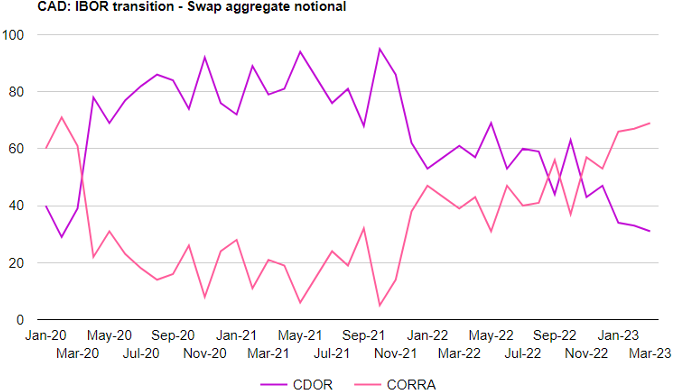

CAD Swaps

Background:

Canada is taking a multiple rate approach. Reformed/enhanced CORRA will continue alongside the incumbent CDOR.

CDOR continues to dominate swap volumes, but CORRA has progressed strongly in Q1 2023 with a record share of trade count at 28% of CAD swaps executed in March 2023. That is nearly triple its historic levels.

In notional traded terms CDOR has been the majority since November 2022 with March 2023 marking a new record of almost 70%.

Conclusion

As the transition of USD-LIBOR approaches, despite the evident progress to date, their remains much to be done in the time remaining. With the experience gained in other currencies such as GBP, EUR, CHF and JPY the industry is well placed to ensure smooth transition.

For more information contact us.